Resources

Blog

Perspectives on financial planning, budgeting, and forecasting.

Read our thoughts on important finance topics for FP&A professionals.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Workforce Planning

Centage

FP&A Software

May 22, 2025

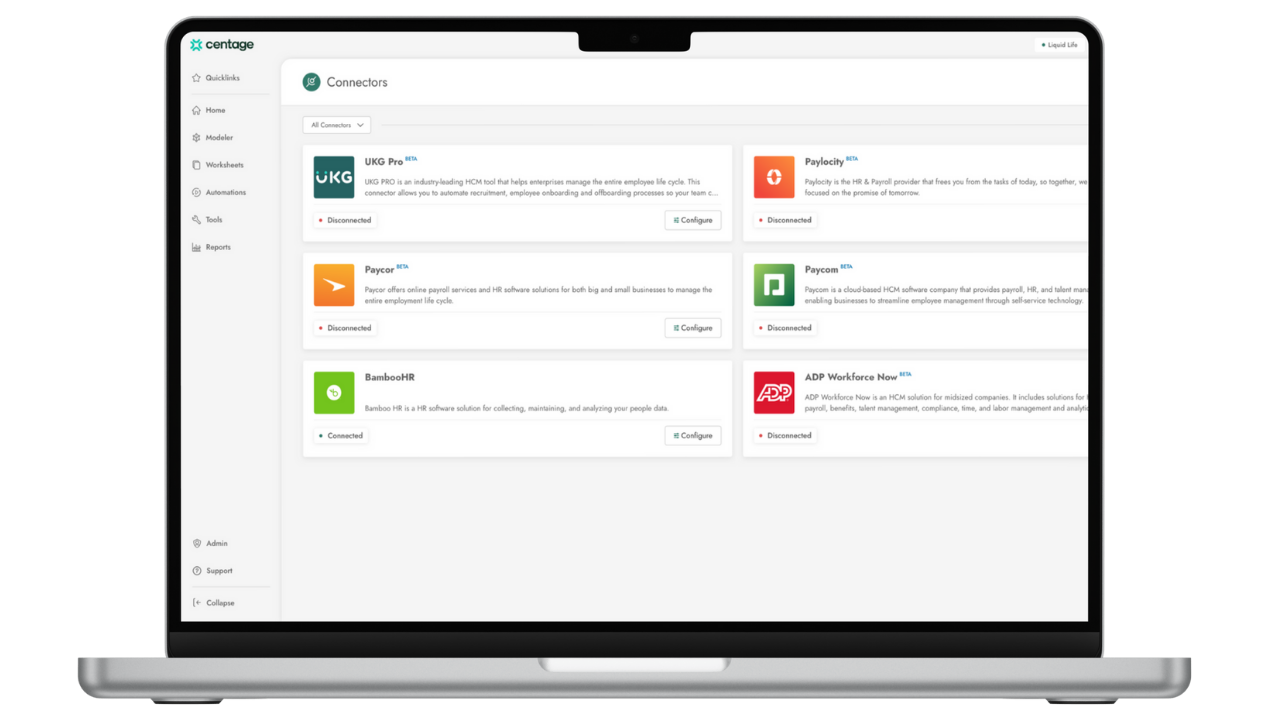

Payroll Integrations Are Live: Real-Time Workforce Data, Zero Spreadsheets

Thought Leadership

Scenario Planning

April 28, 2025

How to Calculate the ROI of AI: A Guide for Finance Leaders (2025 Edition)

Centage

Scenario Planning

Thought Leadership

April 9, 2025

How to Financially Model the Impact of Tariffs (2025 Edition)

Centage

FP&A Software

April 7, 2025

From Spreadsheets to Superpowers: Introducing the New Centage Worksheets

Centage

FP&A Software

Budgeting

Forecasting

Reporting

April 2, 2025

Top 10 Financial Performance Management (FPM) Software Tools for 2025: Features, Comparisons, and How to Choose the Best One

Centage

FP&A Software

Thought Leadership

March 20, 2025

I Crowdsourced the Challenges FP&A Teams Are Having with Excel—Here’s What I Found

FP&A Software

Scenario Planning

Thought Leadership

March 17, 2025

How to Build a Financial Model: A Step-by-Step Guide for Finance Teams

.png)

FP&A Software

Forecasting

February 28, 2025

Smarter Forecasting, Stronger Decisions: How Modern FP&A Tools Drive Success

.png)

Forecasting

FP&A Software

February 20, 2025

Top Financial Forecasting Software Compared: Features, Strengths & Trade-Offs

.png)

.png)

.png)

Budgeting

Centage

FP&A Software

February 5, 2025

Budgeting Nightmares & How to Avoid Them: Lessons from FP&A Experts

.png)

.png)

.png)

Budgeting

FP&A Software

January 28, 2025

Budgeting Together: Tools and Best Practices For Collaborative Budgeting

.png)

.png)

.png)

.png)

.png)

Scenario Planning

Budgeting

January 2, 2025

New Year, New Goals: 5 Key Priorities for FP&A Professionals in 2025

.png)

.png)

Forecasting

FP&A Software

December 11, 2024

Breaking Free from Annual Budgets: Why Rolling Forecasts Are the Future

.png)

Budgeting

Forecasting

Scenario Planning

December 3, 2024

Get Your Master’s in Education Budgeting: A Crash Course for Financial Success

.png)

Budgeting

FP&A Software

Workforce Planning

November 18, 2024

The Budgeting Dojo: Mastering Financial Moves in Manufacturing

.png)

Budgeting

Workforce Planning

Forecasting

November 7, 2024

Don’t Forget This Key Change in Workforce Planning for 2025: New Social Security Wage Base

.png)

Budgeting

Forecasting

FP&A Software

November 1, 2024

5 Proven Strategies to Make Budgeting & Forecasting Less Painful for CFOs

.png)

Budgeting

October 29, 2024

Warding Off Financial Frights: Strategies for Secure and Collaborative Budgeting

.jpg)

.png)

.png)

.png)

.png)

.jpg)

No Results Found

Reset Filters